Blog

EMV Apocalypse Now

This year's EMV liability shifts will radically change the retail ISO landscape by 2018. How do we know? Because we've seen this movie before, played out in other mature post-EMV markets.

May 26, 2016 by atm Atom — blogger, atmatom

ChatGPT

ChatGPT Grok

Grok Perplexity

Perplexity Claude

Claudeby Daryl Cornell, Triton Systems

Shortly after Oct. 1, ATM chargebacks in the U.S. will begin flowing to non-EMV terminals, lawsuits will multiply and tens of thousands of non-EMV ATMs will simply be turned off.

The number of U.S. retail ATMs in operation will seriously contract, possibly forever. Some ISOs will go bust under the weight of crushing chargebacks. Others will consolidate, leaving the large, national ISOs and a handful of nimble, local competitors.

In short, the retail ISO landscape will be radically different by 2018.

How do we know? Because we’ve seen this movie before in the U.K., South Africa and, most recently, Canada — all mature, post-EMV ATM markets.

So what else can we look forward to in the next 24 months?

New ATM sales will dry up

The U.S. retail ATM land rush is long gone. Plummeting hardware prices over the last decade have tripled the number of retail ATMs, many in locations with 100 or fewer monthly transactions.

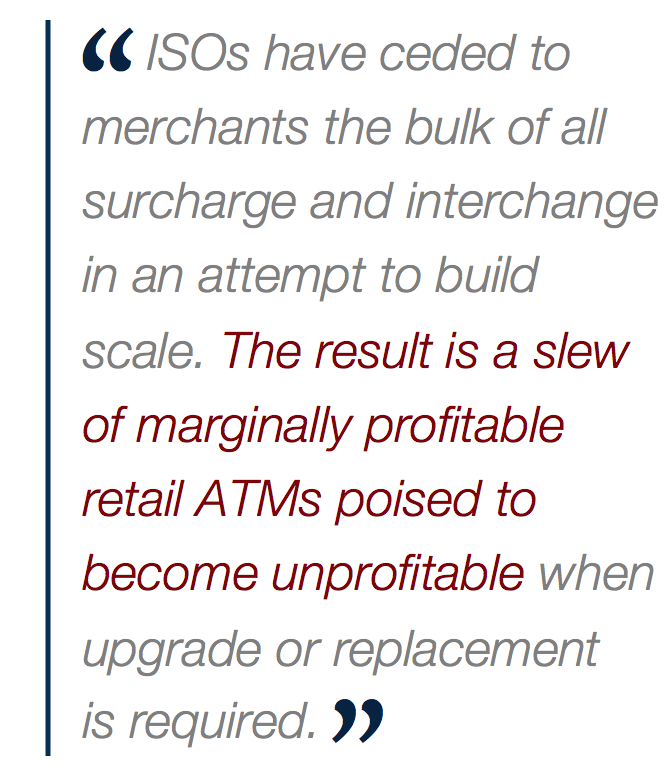

At the same time, most ISOs have ceded to merchants the bulk of all surcharge and interchange in an attempt to build scale. The result is a slew of marginally profitable retail ATMs poised to become unprofitable when upgrade or replacement is required.

As we’ve seen before around the world, once the ATMs at good sites are upgraded or replaced for EMV, new ATM sales will fall by as much as 90 percent — forever.

Surplus ATMs will be everywhere

Industry estimates vary, but somewhere between 10 percent and 40 percent of all U.S. retail ATMs will go dark in the wake of the EMV liability shifts.

This will leave between 25,000 and 100,000 U.S. ATMs piled up in warehouses or sent to landfills. Many of the mothballed ATMs will be harvested for parts eventually, others will be refurbished and resold.

These surplus ATMs will reappear in many low transaction sites, putting additional downward pressure on new ATM sales.

ATM suppliers will exit the US market

Manufacturing is a business in which profitability depends largely on sales volumes. Stable or growing product sales result in lower component purchasing and manufacturing costs.

When new product sales crater — as they will soon in the U.S. — inventory quickly builds and prices drop in the short term as manufacturers flush product.

When this fails and the losses grow, manufacturers rationally exit markets, taking installed product support with them. This has been true in every post-EMV ATM market and the U.S. will not be an exception.

Surviving ISOs will share several traits

A proactive approach to managing EMV liability shift risk will separate the survivors from the many ISO casualties.

Operational excellence will become more critical than ever for viability in a mature, contracting retail ATM industry.

And finally, deep vendor relationships will determine whether your fleet remains viable when the crunch comes. Your suppliers had better be partners if you are to succeed in the post-EMV world.

illustration istock

This article was republished, with permission, from the Triton blog, atmAToM.

About atm Atom

Included In This Story

Triton Systems

Triton FI based products • NO Windows 10™ Upgrade • Secured locked down system that is virus/malware resistant • Flexible configurations - Drive-up and Walk-up • Triton's high security standards • NFC, anti-skim card reader, IP camera and level 1 vaults are all options • Triton Connect monitoring • Lower cost

Subscribe

Get the latest news and resources from ATM Marketplace.

Recent Posts