Article

A tipping point for check imaging?

Check imaging: More growth is on the way.

May 21, 2007 by Tracy Kitten — Editor, AMC

ChatGPT

ChatGPT Grok

Grok Perplexity

Perplexity Claude

Claude*About the author: Peter Kulik is the new technologies product manager forFifth Third Processing Solutions. He is a regular trade-press contributor and industry speaker who has 20 years of experience in the ATM and banking industries. To comment about this commentary, pleasee-mail the editor.

Tipping point: "The magic moment when an idea, trend or social behavior crosses a threshold, tips, and spreads like wildfire."

So writes Malcolm Gladwell in "The Tipping Point - How Little Things Can Make A Big Difference." Put another way, what does the world of Check 21 have in common with crime in New York City, Hush Puppies shoes, or the Midnight Ride of Paul Revere?

Most are familiar with how, in the wake of the events after Sept. 11, the Check 21 Act (Check Clearing for the 21st Century Act) legalized the use of substitute checks - thus removing the dependency on transportation systems to move physical paper for check clearing.

| ||||||||||||||||||

Has the check-processing industry reached a tipping point? Volume growth in check imaging in 2006 has been amazing, even to most industry insiders.

Some recent highlights from the Federal Reserve/ECCHO study:

- Check-21 enabled volume (substitute checks and image exchange) grew 726 percent in 2006; image exchange grew an astounding 3,160 percent.

- The percentage of routing and transit numbers, also known as R/Ts, receiving image files more than doubled to nearly 6,000, representing 34 percent of U.S. financial institutions.(Each FI must have at least one R/T. The check-processing industry has been tracking growth according to the number of R/Ts receiving image files, rather than the number of FIs receiving image files.)

- The value of images exchanged reached 21 percent of total check processing value in December 2006 on an annualized basis, and comfortably exceeded the combined value of debit and credit card payments.

- Image exchange volume exceeded substitute check volume for the first time in September 2006.

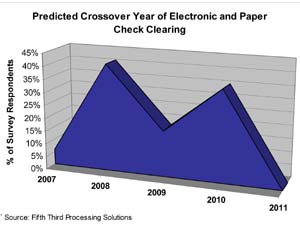

In a December 2006 survey conducted by Fifth Third Processing Solutions, FIs were asked, "In what year do you believe that electronic clearing volume (image exchange and ACH conversion) will surpass paper check volume?" The most common response from FIs was 2008, while responses from the media put 2009 as the year of electronic-check clearing.

|

Peter Kulik |

In that survey, 47 percent of respondents were using image cash letters during the fourth quarter of 2006, and 60 percent were capturing images in one form or another.

But has the industry reached a "tipping point"? Is the industry at a point when steady growth has suddenly become exponential growth?

In 2007, rapid progress has continued, with some key events:

- Image volume has continued to grow to 20 percent of annualized items and 24 percent of annualized value in March 2007.

- 41 percent of R/Ts were in March enabled for image files.

- In the four-month period spanning September 2006 to January 2007, check-image exchange volume more than doubled - growing 111 percent.

And, perhaps more importantly, Viewpointe and Endpoint Exchange announced a link to exchange images in November 2006. In addition, Endpoint Exchange and SVPCo announced a link to exchange images in April 2007.

And, perhaps more importantly, Viewpointe and Endpoint Exchange announced a link to exchange images in November 2006. In addition, Endpoint Exchange and SVPCo announced a link to exchange images in April 2007.

Based on industry events, it seems clear that we have reached a "tipping point" for check-image processing expectations.

Talking to FIs and reviewing the trade press, it seems that the industry is no longer questioning "if" check imaging and image exchange will take off, but, rather, "when" it will happen. Driven by remote capture, price increases from the Fed, and the favorable economics of image exchange, we believe there will be no turning back to paper-check processing.

On the other hand, while image-exchange volume growth has been strong, it has not been exponential. Analogous to EFT debit networks in the 1980s, the constraint may be the operations of image-exchange networks, which will change dramatically with the recent reciprocal agreements between Viewpointe, Endpoint Exchange and SVPCo.

The potential for ATM check imaging has yet to be realized, but the economics will get much stronger as the image-exchange infrastructure continues to develop, saving transportation costs for remote deposit ATMs. Further, remote capture of check images has a strong return on investment and will continue to drive increased volume of check images to fuel growth in image exchange.

So, have we reached a tipping point for Check Imaging? The data suggests a tipping point is imminent - so hold on for a continued wild ride in 2007.

Mike Walter and Hideo Core of Fifth Third Processing Solutions contributed to this article.

Banking Executive SummaryDepositsTrends / StatisticsTransaction ProcessingEFT NetworksOtherNorth AmericaBank / Credit UnionVantiv

Related Media

Featured Vendor

![]()

In business for more than three decades, Lock America, Inc. of Corona,CA develops, manufactures and markets high security locks for various industries, including amusement, gaming, information management, fuel distribution and self-storage.

Subscribe

Get the latest news and resources from ATM Marketplace.