Article

First look: 2018 ATM and Self-service Software Trends

The ATM industry's most popular report was released today and is now available for free download. Here's an excerpt ...

October 25, 2018 by Suzanne Cluckey — Owner, Suzanne Cluckey Communications

ChatGPT

ChatGPT Grok

Grok Perplexity

Perplexity Claude

ClaudeEditor's note: Yesterday, ATM Marketplace andKAL ATM Softwarereleased the 11th annual edition of ATM and Self-service Software Trends report, an investigation of current and emerging directions in ATM and self-service device functionalities and the software that supports them.

To coincide with the release of the report, ATM Marketplace and KAL shared highlights from the survey in a free one-hour webinar, nowavailable for replay.

The following is an excerpt from the 2018 report, which isavailable for download.

The Incredible Shrinking Branch Network

The number of bank branches in the United States peaked in 2009.

Then, amid a major global financial crisis and a massive increase in the number of internet and smartphone users who found branch visits less necessary — and less convenient — the numbers began to fall.

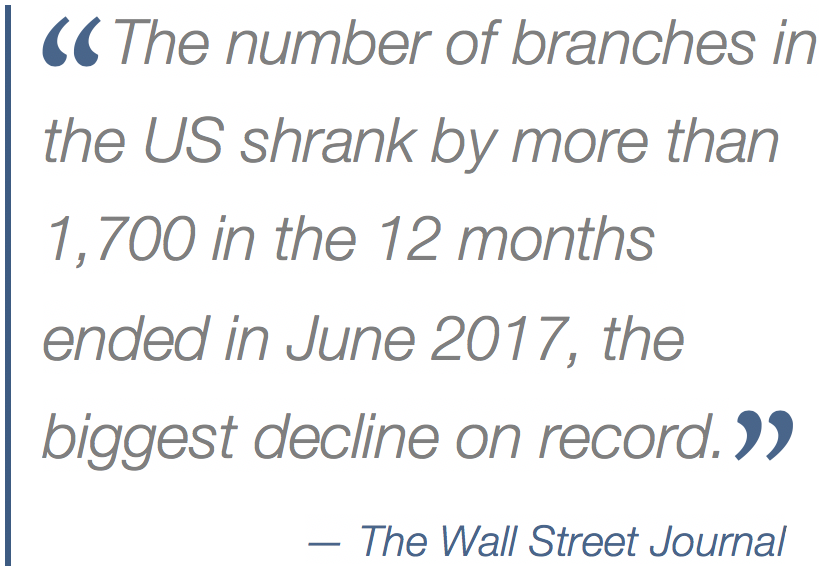

According to the St. Louis Fed, "Since 2009, the number of commercial bank and thrift branches has shrunk nearly 10 percent, or just over 1 percent per year."

In the period from mid-2012 to mid-2017, many regional US banks significantly reduced their branch footprint:

- Capital One Financial Corp. cut 32 percent of its branches.

- SunTrust Banks Inc. cut 22 percent of its branches.

- Regions Financial Corp. cut 12 percent of its branches.

In total, U.S. banks have shuttered 9,000 branches in this decade. Smaller community banks have notably bucked the closure trend, either growing or at least maintaining branch networks, but the net numbers are negative, and substantially so.

In other mature markets the story is the same. The U.K. has been hard hit with branch closures in recent times, with 3,000 shuttered within the past three years.

Former Barclays chief executive Antony Jenkins has predicted that half of the U.K.'s remaining 7,000 branches could disappear within the next five to 10 years.

In Europe, the theme continues. Since 2008, 48,000 branches have closed across the European Union, according to the European Banking Federation. That's more than 20 percent of all EU bank branches.

Anyone presuming that this was simply due to the economic crisis would be mistaken. More than 9,000 banks closed in 2016, seven years after the end of the Great Recession.

In almost all cases — especially in smaller communities — the primary reason cited for closures has been that of significantly decreased footfall resulting from a dramatic increase in online and mobile banking.

In almost all cases — especially in smaller communities — the primary reason cited for closures has been that of significantly decreased footfall resulting from a dramatic increase in online and mobile banking.

Banks argue that they simply cannot justify the continued expense of operating branches to accommodate a fast-shrinking number of customers — the majority of them older people — whose preference is to bank face-to-face with a live teller.

And despite frequent assertions from various quarters that millennials — and now Gen Z — still want personalized banking with a human touch, the fact remains: Branch traffic has declined — more than 45 percent over the past 20 years — and will continue to decline — an additional 36 percent between 2017 and 2022, per predictions.

A stand-in for the branch

All of this bodes to make the ATM channel even more important to the banking sector in the decades to come than it has been in the first 50 years of its existence.

Says Korala: "If you ask me what was priority No. 1 for banks over the last 10 years, it would be cost reduction. But now I'd say that has fallen further down on the list."

In fact, as recently as 2016, cost reduction ranked No. 1 in the list of critical changes survey respondents said their institutions needed to make to ATM operations.

In the 2017 study, cost reduction was respondents' second priority, tied in importance with the need to migrate in-branch transactions to self-service systems.

In 2018 respondents put cost reduction in fourth place — tied at 18 percent with cash-handling efficiency.

However, Korala pointed out that today's financial institutions are looking at a broader cost reduction picture — one whose centerpiece is the rationalization of branch networks and shuttering of underutilized branch locations.

|

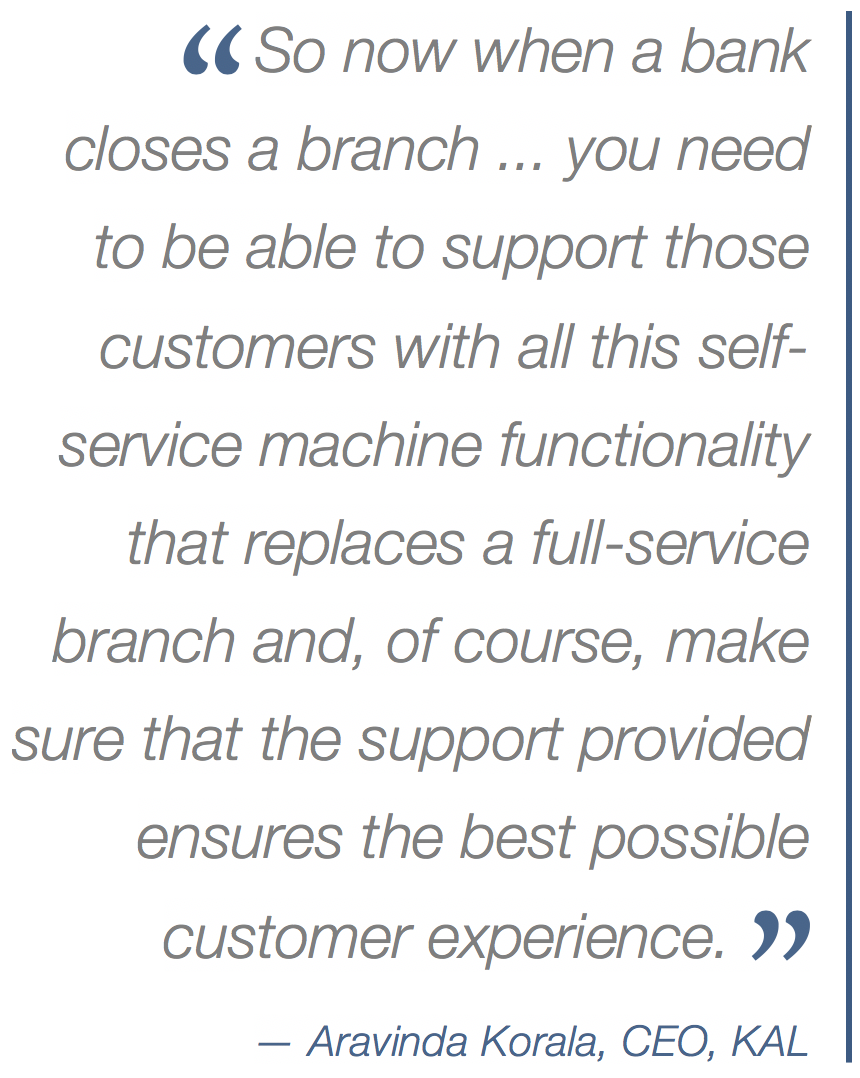

"So now when a bank closes a branch it's about replacing the branch with an ATM or a kiosk," Korala said. "You can think in terms of a 'gray scale' of hardware, starting from maybe some really low-cost machines on one end and really high-performance devices on the other end, depending on the location and the services most customers will need.

"And you need to be able to support those customers with all this self-service machine functionality that replaces a full service branch, and of course make sure that the support provided ensures the best possible customer experience.

"Instead of ATM cost reduction what I would put at No. 1 is a bigger picture of cost reduction focusing on branch transformation or branch substitution through self-service."

Ultimately, financial institutions must ensure that their customers feel just as comfortable at a self-service machine as they would at a teller window.

The dawning realization of this fact has led financial institutions to elevate the importance of customer experience — from No. 3 in the 2016 ATM and Self-Service Software Trends survey — to No. 1 in 2017 and No. 1 again in 2018.

About Suzanne Cluckey

Suzanne’s editorial career has spanned three decades and encompassed all B2B and B2C communications formats. Her award-winning work has appeared in trade and consumer media in the United States and internationally.

Included In This Story

KAL ATM Software

KAL software delivers ATM efficiency and innovation you can bank on. It powers over 350,000 ATMs and dispenses more than $1 trillion per year.

Related Media

InnovationPresented ByHyosung

Subscribe

Get the latest news and resources from ATM Marketplace.