Commentary

NAC serves up a new ATM survey and spins an old fallacy

The National ATM Council has repeatedly said that big banks control FICO and use it as a propaganda tool to make retail operators look bad. Yet, the hard data they use to back up their claim actually proves them wrong.

May 18, 2017 by Suzanne Cluckey — Owner, Suzanne Cluckey Communications

ChatGPT

ChatGPT Grok

Grok Perplexity

Perplexity Claude

ClaudeA week or so ago, the National ATM Council circulated a press release announcing the findings from its second annual survey of independent ATM operators in the United States. They also used the release as an axe-grinder, repeating for the umpteenth time a fact about big banks that isn't factual at all.

But first, the survey.

The 2017 U.S. Retail ATM Skimming Survey appears to have asked the same questions and applied the same unscientific methodology to produce roughly the same results as the 2016 survey:

- 90 percent of respondents had not found a skimming device on one of their ATMs in the last 12 months;

- 89 percent routinely checked for skimmers;

- 87 percent provided a number for an ATM user to call in case of an irregularity at the machine; and

- 70 percent had been in business for at least 10 years.

Only two of these questions are remotely informative in relation to the topic of skimming of payment card data at retail ATMs over the past year: The third question is irrelevant without a follow-up asking how many times the phone number was used by a consumer reporting a suspected skimmer; and the fourth question is immaterial, since the survey was only concerned with a one-year time period.

Assuming that FICO releases another skimming update in 2018, and that NAC responds with a third annual survey, it would be more, oh, I don't know ... scientific? ... if they were to expand their polling (and reporting) with a few basic questions:

- size of respondents' ATM fleets;

- distribution of respondents' ATM fleets;

- extent of losses linked to compromised ATMs;

- percentage of ATMs that are/are not EMV enabled; and

- percentage of ATMs at attended and unattended locations.

Back to the press release.

NAC applauded FICO for acknowledging in an earlier story by ATM Marketplace that "a very small percentage" of U.S. IAD-operated ATMs was compromised last year.

With that, it was beginning to seem as though NAC might be ready to move on from their deny-and-discredit campaign against FICO. Except they weren't.

The very next paragraph included this comment from NAC Vice-Chairman Patrick Conner of ATMPartMart.com:

NAC has been unable to reconcile FICO's recent contentions that it is not owned by banks. A quick review of NASDAQ's listing of FICO's largest shareholders shows that several of the largest U.S. depository institutions, Bank of N.Y. Mellon Corp., JPMorgan Chase, Bank of America and others are listed as major shareholders that own large amounts of FICO stock.

This deserves an Anderson Cooper-worthy eye roll, as it's a question that had been addressed definitively in an April 18 interview by ATM Marketplace, and, 10 days later, in a blog where it was pointed out that:

FICO's largest shareholders are the institutions and funds listed here, information that's as easy to find as typing 'Who are FICO's major shareholders?' in your browser bar, which NAC apparently has not tried.

Well, apparently, NAC eventually did decide to try it. Their search turned up a link to Nasdaq, which I must admit, provided far better information than my link to Morningstar.

It was enough information to suggest upon "quick review" that NAC's conclusion probably was wrong and in fact, with a few hours of basic mathematics and background research, to prove that it absolutely was wrong, as shown below:

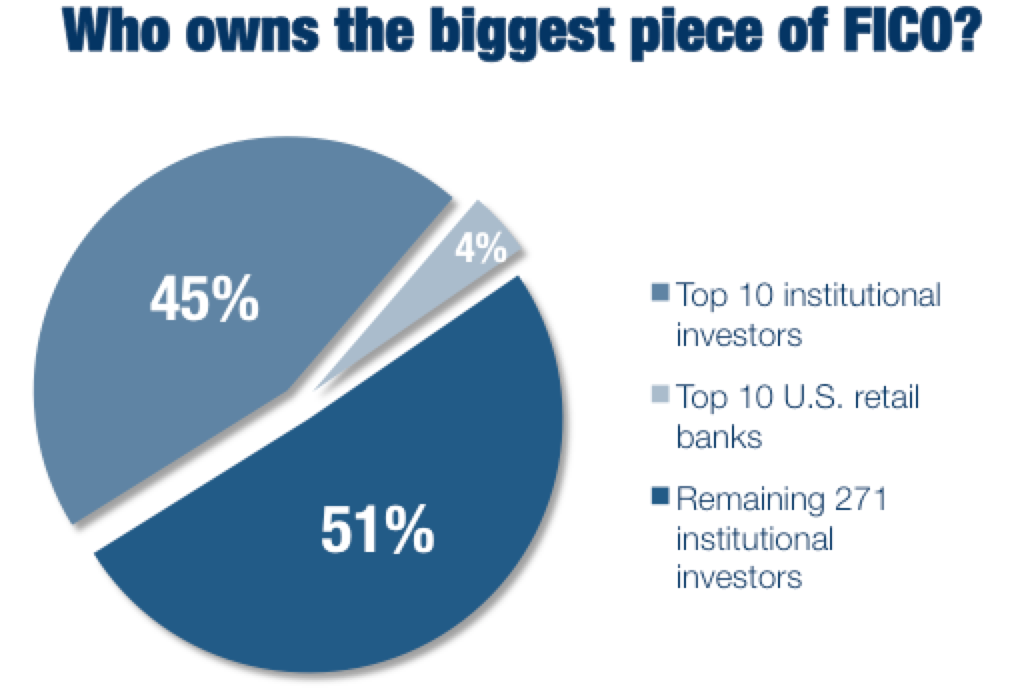

Granted, 1.27 million shares is "a large amount of FICO stock." But, as shown above, it still represents less than one-tenth of the shares held by the 10 largest FICO institutional investors — hardly a controlling interest, even assuming a heroic effort at collusion by the top 10 U.S. retail banks.

Further, of a total of 31.3 million shares owned by all 291 of FICO's institutional investors, the slice held by these top 10 banks represents just 4 percent of the pie. The figure approaches statistical insignificance.

|

By way of comparison, the number of U.S. retail ATM operators surveyed by NAC who reported finding a skimmer on one of their machines, at 10 percent, a number that NAC itself dismisses as "very low."

What it really comes down to though, is this: The question of FICO ownership amounts not to much ado about nothing, but to "much ado about the wrong thing."

The existential threat to independent operators isn't FICO and financial institutions of whatever size.

The real and imminent threat is the risk run by all non-EMV ATM operators of being dumped by processors or decimated by a well-executed skimming attack once the final implementation deadline passes in October.

Under these circumstances, promoting an IAD vs. FI mentality just isn't helpful.

U.S. banks and independent ATM deployers have always had a symbiotic, if complicated, relationship. They need one another. And as ATM operators, they share the same purpose — or should, anyway: to advocate for and provide reliable, safe and seamless consumer access to cash. It really is that simple. Now can we move on?

A seven-page report available for free download at NATMC.org, presents the polling results and a few comments from survey participants — and not much else.

About Suzanne Cluckey

Suzanne’s editorial career has spanned three decades and encompassed all B2B and B2C communications formats. Her award-winning work has appeared in trade and consumer media in the United States and internationally.

More From CommentaryMore

SecurityPresented ByDiebold Nixdorf

Subscribe

Get the latest news and resources from ATM Marketplace.

Recent Posts