Article

Latin American ATM market on the upswing

While Latin America's ATM market has lagged behind North America and Europe for the past several years, a new report by Speer & Associates predicts strong growth in the region for the next three to five years.

November 7, 2001

ChatGPT

ChatGPT Grok

Grok Perplexity

Perplexity Claude

ClaudeWhile Latin America has not been a hotbed of ATM activity in the past decade, some industry analysts expect the market to warm considerably during the next few years.

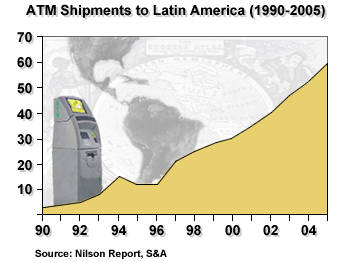

A recently-issued report by the Atlanta-based consultancySpeer & Associates, "Leveraging ATMs in Latin American Distribution Channels: Past, Present and Future," predicts that the region will see ATM deployment increase 6-8 percent for the next three to five years.

"The proliferation of ATMs is remarkable. There's just a huge emphasis on cards," said Marilyn Parker, an S&A vice president and author of the study, noting that issuance of ATM and debit cards grew by about 70 percent in 2000.

Figures from industry newsletter the Nilson Report support Parker's contention. According to Nilson, ATM shipments in 2000 totaled 30,000 terminals, 19 percent of world shipments.

If one part of the region experiences a drop in deployment – because of a downturn in the local economy, for example -- other areas tend to take up the slack.

|

"It's a very steady market if you look at it regionally rather than country by country," Parker said. "Unlike the U.S., when one of the markets is off, some of the others invariably pick up."

Foreign players

Several factors are contributing to the uptick in ATMs, Parker said, including the entry of foreign financial powers like Citibank, which purchased Banamex-Accival, one of Mexico's largest financial groups, for $12.5 billion U.S. earlier this year. "Across the region, there are relatively few local banks left," she said.

Foreign players are making a strong push to increase the card base, Parker said, which gives the dwindling number of local banks an incentive to follow suit. "The local banks have done a good job of going after new markets, but (new entrants) will make them step up to the plate and be even more competitive."

One of the region's traditional challenges has been a high percentage of Latin Americans without bank accounts, but Parker said this is beginning to change. In addition to aggressive marketing by foreign corporations, she identified bank-at-work programs as a major impetus for moving the unbanked toward banking relationships.

Under these programs, which are sometimes mandated by government entities, companies establish accounts into which they can directly deposit workers' salaries. According to Parker, some have even installed ATMs at work sites and taught employees how to use them. Mexico's Bank Bital has partnered with several large corporations on such programs, she said.

Others have reached out to the unbanked by introducing branches and ATMs in non-traditional locations. Argentina's Banco Galicia, for instance, has placed ATMs in post office branches, Parker said.

Despite those efforts, Parker believes remote ATM deployments represent a major opportunity for financial institutions. "There's not good coverage outside of major metro areas. That's one are they should be looking at," she said.

Unlike other areas of the globe where independent deployers have taken the lead in remote deployment, Parker said ISOs are largely a non-factor in Latin America because of formidable barriers of entry erected by financial institutions. "Their presence is minimal at best," she said. "The banks have really shut them out."

Parker doesn't believe that surcharging will be introduced anywhere in Latin America in the near future. Interchange is fluid across the region, she said. "It varies hugely from country to country, depending on network linkages."

Network news

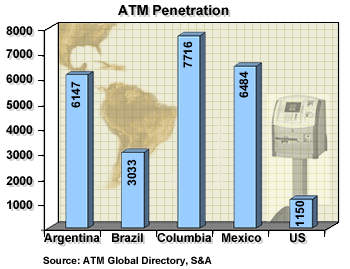

One of the region's biggest remaining challenges is its inconsistent network interconnectivity. Chile has what Parker calls "one of the most efficient and effective networks in the Southern Hemisphere," with shared network Redbanc processing transactions for all of the commercial banks. Brazil, in contrast, offers very little interconnectivity – even though it's the largest ATM market in the region with more than 80,000 machines.

|

While the situation is improving, Parker said, some banks are reluctant to negotiate because they believe they would give up a competitive advantage by establishing more linkages.

Brazilian bank Bradesco, for instance, maintains a proprietary network of 20,000 machines. Because it already has such high market penetration, Bradesco does not want to join the local switch, Banco24Horas.

Helllloooo out there?

Another challenge is telecommunications. While the overall infrastructure has improved dramatically since privatization of the industry, some areas still suffer from high costs and low efficiency, Parker said. "It's probably the single most important factor in getting all of this to work."

In areas where telephone lines are scarce, Parker said that wireless connections offer an option.

Fraud is a bigger problem in Latin America than in North America or Europe. Parker said some banks are adopting the use of software that allows cardholders who are being victimized to type in an alternate PIN to alert police that a robbery is occurring.

Tech talk

Parker said Latin America's largest financial institutions are increasingly adding technology to their ATMs. Banamex, Mexico's largest bank (now owned by Citibank), recently purchased 500 Web-enabled ATMs from Diebold Mexico, Parker said, and plans to install them in areas where both education level and income per capita are above average.

Other advanced ATM functionality in which Latin American banks have expressed interest: money transfers, advertising and sale of airtime to mobile phone users.

"The next big wave," Parker predicted, will be enhanced CRM (customer relationship management) tools.

"I believe the banks want to know who is using their ATMs and why," she said. "They're very interested in taking that information and offering targeting marketing at the ATM."

Included In This Story

Diebold Nixdorf

As a global technology leader and innovative services provider, Diebold Nixdorf delivers the solutions that enable financial institutions to improve efficiencies, protect assets and better serve consumers.

Related Media

Subscribe

Get the latest news and resources from ATM Marketplace.