Article

As ATM sales slump through H1, NCR hangs its hat on H2 gains

The company saw a year-over-year downturn of 21 percent in Q2 ATM revenues, but says Q4 projects, expanding profit margins and growth in its software and services segments will see NCR through to the end of 2017 with its full-year earnings forecast intact.

July 25, 2017 by Suzanne Cluckey — Owner, Suzanne Cluckey Communications

ChatGPT

ChatGPT Grok

Grok Perplexity

Perplexity Claude

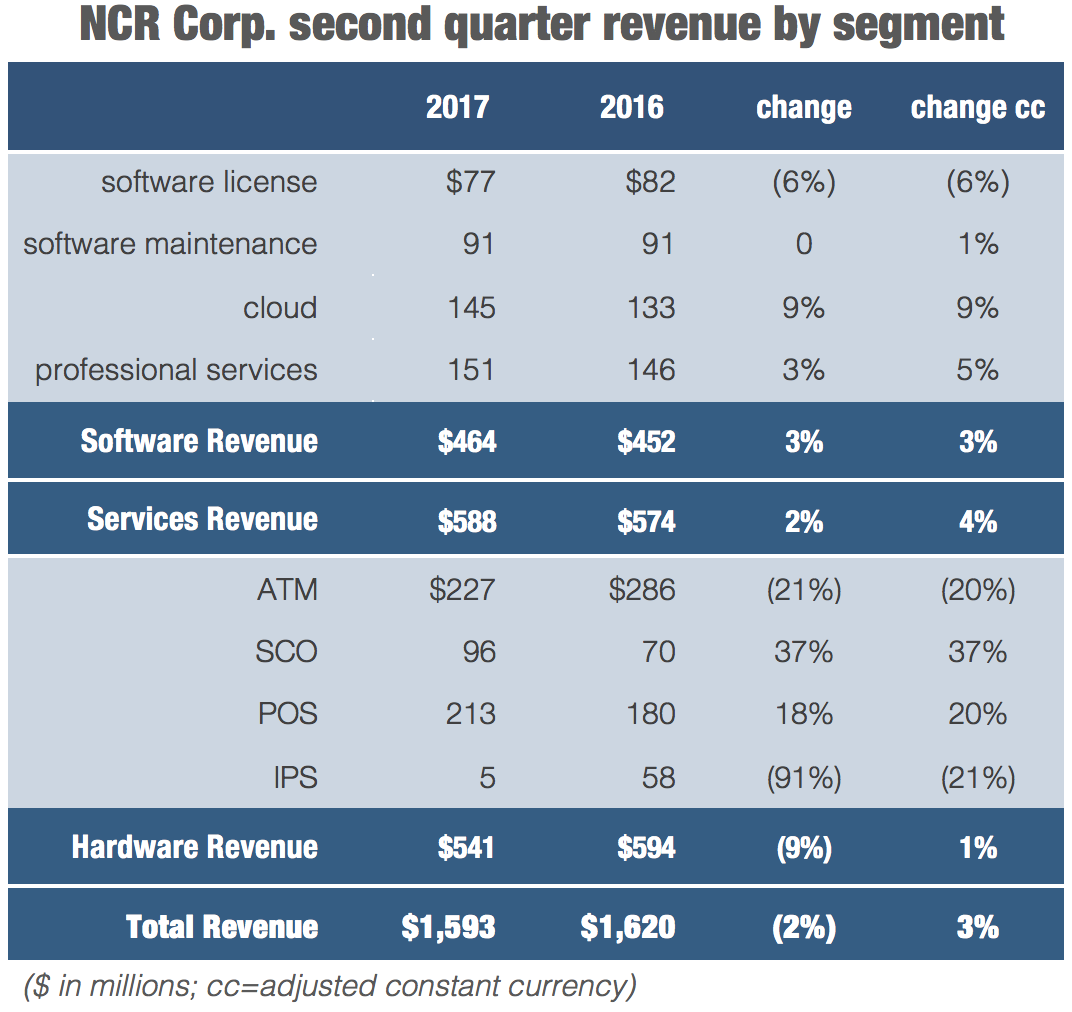

ClaudeWith ATM sales slumping more than 20 percent in Q2, NCR Corp. has a considerable task cut out for it if the company is to meet its full-year revenue objectives. Earnings for the quarter were down overall and weak hardware sales were the chief culprit.

|

President and COO Mark Benjamin told analysts on in the Thursday afternoon earnings call that he remains confident in the company's ability to overcome the deficit in the first half of 2017. He explained that ATM revenue is expected to improve in Q4 as the company completes scheduled rollouts for some of its larger customers.

Following prepared remarks that made only a glancing reference to a $59 million year-over-year decline in ATM revenues — from $286 million in 2016 to $227 million in 2017 — Benjamin and other NCR executives took a grilling about their full-year forecast from analysts during the Q&A segment of the call.

As one analyst pointed out, based on its current projections for Q3, the company will be pushing an projected $70 million of earnings into the fourth quarter. This will entail sequential growth of 15 percent, compared with a norm closer to 6 percent in the past three years.

Benjamin said that despite "just a little bit of softness" in the second and third quarters, "The backlogs are still good. The order flow is still good. Our customers are buying from NCR. We are taking share in the market and our conversions will take hold in the back half."

Perhaps the heaviest drag on the company's ATM revenue has been demonetization in India, a market that NCR dominates in ATM sales and service. After 500 and 1,000 rupee notes were declared invalid last November, banks and independent deployers found themselves unable to procure replacement 1,000 and 2,000 rupee notes in quantities large enough to meet customer demand.

As ATM surcharge fees subsequently declined due to outages, so too did ATM spending by FIs and IADs. However, as the cash situation finally begins to stabilize, it seems likely that the Indian ATM market will bounce back. Despite a government initiative pushing cashless transactions, demand for folding money remains strong in that market.

Another factor in NCR's dismal ATM sales was weak demand in mature markets, a continuing trend that NCR and Diebold Nixdorf both observed in earnings calls last week.

Benjamin said that NCR management anticipates a bump in demand as financial institutions upgrade their ATMs in anticipation of the industry's pending migration to Windows 10. However, this lies well in the future, as Microsoft support for the current Windows 7 operating system is not scheduled to end until January 2020.

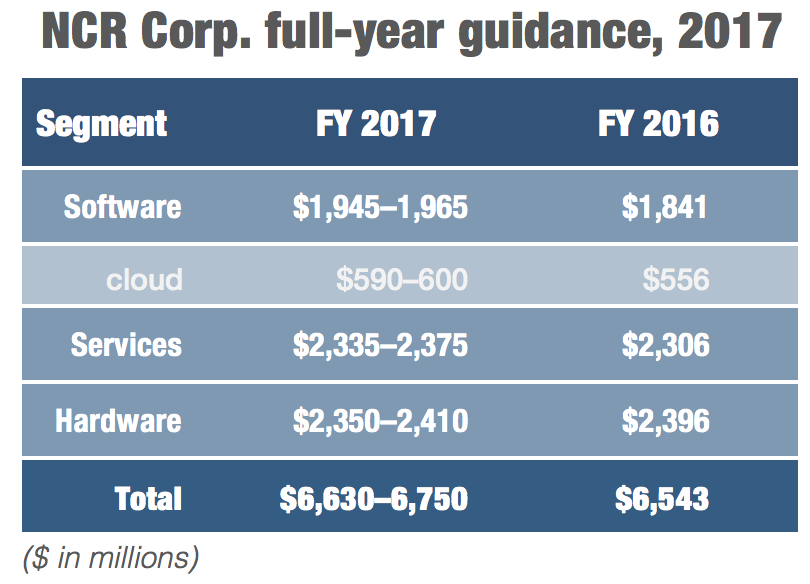

Fortunately for NCR, the company has diversified in recent years in its pursuit of an omnichannel business model. And the performance of non-ATM hardware at NCR mostly saw improvement in Q2, encouraging the company to project full-year growth for the segment at 3–6 percent in constant currency.

"We are clearly benefiting from the diversity of our revenue streams from both a solution and market perspective which has kept us on track to achieve our full-year guidance," Benjamin said in his opening remarks.

Software was a particular bright spot in the quarter, he said. "Our software revenues continue to expand, including 9 percent growth in cloud revenues along with a 13 percent increase in net [annual contract value]. We have built a roughly $2 billion software business including almost $600 million in cloud revenues coming from customers across financial, retail and hospitality markets."

Executives were also pleased with quarterly results in the services division, where reorganization efforts have paid off in the form of greater efficiency, productivity and customer loyalty, Benjamin said.

NCR services revenue grew from $574 million to $588 million year over year. While this amounts to quarterly growth of only 2 percent (or 4 percent in constant currency), improvements in efficiency and a higher-value service mix combined to improved the non-GAAP gross margin in Q2 a whopping 20 percent (24 percent in constant currency).

The company expects to continue margin growth along several lines, including a higher mix of managed services; further productivity and efficiency improvements; remote diagnostics and repair capability; and product life-cycle management, according to prepared remarks by NCR CFO Bob Fishman.

"Our investment in big data analytics, predictive monitoring and customer onboarding are allowing customer service cases to be resolved more efficiently while reducing dispatches," he said. "Incremental services margin expansion remains a key focus as we execute our strategy."

|

In his closing remarks, Benjamin reaffirmed his confidence in the company's full-year forecast. "We remain a global leader in omnichannel software, channel transformation and digital enablement … our solutions are aligned with major market trends and customer demands and we need to continue innovating in order to maintain our leadership edge and provide customers with competitive differentiation."

Three months from now, we'll all have a better idea how that's panning out.

About Suzanne Cluckey

Suzanne’s editorial career has spanned three decades and encompassed all B2B and B2C communications formats. Her award-winning work has appeared in trade and consumer media in the United States and internationally.

Featured Vendor

![]()

Auriga is a top international software solutions company, specialized in end-to-end systems that integrate the various delivery channels used in retail and internet banking.

Subscribe

Get the latest news and resources from ATM Marketplace.