News

ISOs feeling financial squeeze

A new Dove Consulting study shows that the cost of operating ATMs is rising for large ISOs, bringing their expenses more in line with those of their financial institution counterparts.

November 3, 2002

ChatGPT

ChatGPT Grok

Grok Perplexity

Perplexity Claude

ClaudeISOs have long prided themselves on being lean, mean deployment machines - running their ATM programs in a more cost-effective manner than their counterparts at financial institutions.

However, it looks like ISOs may be carrying some additional financial weight, based on a recent survey conducted by Dove Consulting on behalf of four of the nation's largest EFT networks.

The new study is an update of the Boston-based consultancy's landmark 1999 ATM deployment study. In that study, Dove found that the cost of operating an off-premises ATM averaged $703 a month for independents, compared to $1,090 a month for other deployers. (The 1999 study reflected 1998 costs.)

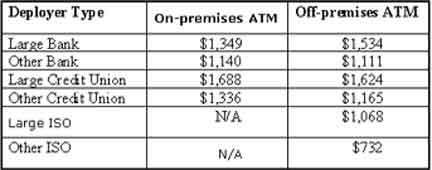

The new study, however, found that large ISOs now have operating costs similar to their counterparts at financial institutions. The average cost for all deployers, according to the study, is $1,298 a month, including rent and back office allocations.

The highest cost is incurred by large credit unions (those with more than $500 million in assets), with a cost of $1,624 per ATM per month. At the low end of the scale are small ISOs (fewer than 1,000 ATMs), with a cost of $732 per ATM per month.

Moving toward the middle

Just 43 dollars separates the large ISO (1,000-plus ATMs) from the smaller bank (less than $10 billion in assets). According to Dove, a large ISO spends an average of $1,068 a month to operate an ATM, while a smaller bank spends $1,111. Banks with more than $10 billion in assets spend more, $1,534 a month.

|

Tony Hayes, director of Dove's Financial Services practice and one of the study's authors, believes several factors are driving cost increases on the ISO side. Large corporations with large expenses - such as American Express, E*TRADE Bank and eFunds - have entered the ISO category, driving up the average cost of operations.

"What is an ISO today?" Hayes said. "It's getting harder and harder to define; there's a growing gray area."

Many of these non-traditional ISOs have a well-known brand to protect, Hayes added. Because reliability and availability are more important to them, they are investing in more sophisticated monitoring and management software. For the same reason, they also tend to spend more on service and maintenance than smaller ISOs.

Feeling the squeeze

Another area in which some ISOs are feeling a squeeze is cash costs. A large ISO's biggest expenditure, Hayes said, is typically cost of funds. "These guys have to buy the money, whereas most banks provide their own cash."

While small ISOs enjoy a significant savings by vaulting the cash themselves or having a merchant do so, Hayes said large ISOs service larger clients such as retail chains - and those businesses want ISOs to take care of all the details, including cash replenishment.

ISOs also typically pay more rent to a retail business to place a machine and/or share a larger percentage of the transaction revenues than a financial institution, Hayes said, largely to counteract the selling power of the bank brand.

"If a merchant is offered a choice between having an ATM from a bank or an ISO and the financial terms are the same, they're always going to choose the bank. They like having that bank brand on their machine," Hayes said. "An ISO is going to have to cut a more aggressive deal."

One expense that typically hits financial institutions harder than ISOs, regardless of size, is depreciation of hardware. Financial institutions deploy pricier, full-function ATMs in retail locations, according to Hayes.

Profits, what profits?

The Dove study also uncovered some surprising numbers in regard to revenue generation. According to the study, large bank deployers generate an average of $1,835 per off-premises ATM per month, more than any other deployer segment.

Hayes notes this is because they tend to secure high-volume locations, employ highly identifiable ATM surrounds and branding, route their transactions through EFT networks with higher interchange rates and charge higher than average surcharge rates (an average of $1.65, compared to an overall average of $1.48).

Because ISOs clock far fewer transactions than financial institutions (an average of 600 a month, compared to 1,918, according to the study), large ISOs earn an average of $806 a month per ATM while smaller ISOs earn an average of $750 a month per ATM.

That means large ISOs experience an average monthly loss of $262 per ATM, Hayes said. Within this category, he added, 60 percent of large ISOs are profitable while the remaining 40 percent are not. All of the deployers in the other ISO category are marginally profitable.

Bruce Kreeger, president of Mine Hill, N.J.-based ATM Center, an ISO with about 1,000 ATMs under contract, doubts some of the Dove numbers. Kreeger said his gross profits are up and net profits are slightly down - but his company is definitely in the black.

Kreeger said he wonders whether some of the 17 ISOs who participated in the study misunderstood some of the questions or, perhaps, fudged a bit on their own numbers (not an uncommon phenomenon in the ISO world).

Noting that several different bank departments are usually involved in running an ATM program, Kreeger said he believes that financial institutions don't always have an accurate handle on the profits and losses of their off-premises machines. "I'd venture to say a lot of banks don't even know their cost of operations," he said.

Crunching the numbers

Hayes identified two major factors to back up Dove's numbers.

First, ISOs reported cost information only on the ATMs that they owned and operated. In contrast to the early years of the retail ATM market, the majority of machines today are owned by merchants, who assume much of the cost burden. "It is probably not surprising that the majority of ISOs have changed deployment strategies and are now more aggressively pursuing the merchant-owned segment of the market," Hayes said.

T.J. Hannon, vice president of marketing for Hanco Systems, a Peachtree City, Ga.-based ISO that last month sold its portfolio of 2,500 ATM contracts to eFunds, agreed that it's tough to turn a profit on many placements as transaction levels continue to decline. "Your fixed costs remain the same whether you do one transaction or one thousand," he said.

ISOs that are still aggressively pursuing placements may do so for reasons other than financial, Hannon added, such as establishing a larger relationship with a corporate client or earning a contract with a "name" business such as Kmart or Holiday Inn.

Second, some of the aforementioned non-traditional ISOs (American Express, E*TRADE) have cardholders of their own, Hayes said, and deployment strategies more similar to those of financial institutions. According to Hayes, these acquirers have expressed their intent to use their ATMs as another distribution channel for their cardholders, so may be willing to accept losses on a channel basis in return for stronger customer relationships and increased profitability on a customer basis.

Because declining transaction volumes and market saturation have resulted in losses for ISO deployers, Hayes noted, some larger players have opted to exit the business.

Hannon agreed with Hayes, although he said that not all consolidation will involve actual acquisitions. "I think even ISOs that aren't looking at being acquired are probably looking a lot more at partnership opportunities," he said.

The Dove study, which was conducted for Co-Op Network, NYCE Corporation,PULSE EFT Association and Star Systems, queried 28 large banks (assets of $10 billion-plus), 34 other banks (less than $10 billion in assets), 25 large credit unions (assets of $500 million-plus), 23 other credit unions (less than $500 million in assets), eight large ISOs (1,000-plus ATMs) and nine other ISOs (less than 1,000 ATMs).

The 82,188 ATMs accounted for in the study represent approximately a quarter of the total United States installed base of 324,000, according to Dove.

Related Media

Cash Dispenser / Recycler / AcceptorPresented ByACG

Vault Cash / Cash ManagementPresented ByCash Connect

Subscribe

Get the latest news and resources from ATM Marketplace.