Article

2002: A year in review

From card fraud to increased regulation, advanced functionality to international expansion, 2002 was another year to remember in ATMs.

January 6, 2003

ChatGPT

ChatGPT Grok

Grok Perplexity

Perplexity Claude

ClaudeIn the world of television, "The Fear Factor" won boffo ratings for NBC by showcasing people who performed bizarre "stunts" that included choking down a variety of dishes designed to disgust, from Madagascar hissing cockroaches to fermented squid guts.

The ATM industry in 2002 found it difficult to stomach an unappetizing fear factor of its own, criminals using increasingly sophisticated methods of illegally obtaining card information and using it to drain funds from cardholders' accounts.

Several seemingly well-organized fraud rings struck around the world. One of the most high profile was a pair of Russian brothers with ties to organized crime and a history of check fraud, who purchased ATMs from ISOs and placed skimming devices inside of them before deploying them in California, Florida and New York in late 2001 and early 2002.

While the Federal Bureau of Investigation made two arrests in the case last January, the alleged ringleader is still at large. At last count, losses had reached about $4 million and 20,000 ATM cards had been recommended for block and reissue.

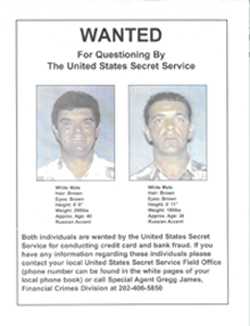

|

The man on the left, the alleged leader of an ATM skimming scheme that the Secret Service believes may have impacted up to 1,400 financial institutions in 2002, is the kind of sophisticated criminal involved in today's card scams. |

According to an address given in November byNYCEExecutive Vice President Susan Zawodniak at theATM Industry Association'sSummit & Awards in San Diego, Calif., other fraudsters targeted bank branch ATMs.

In one case, realistic-looking "ghost" overlays were placed over the fascia of ATMs in the Southeast to gather card data after the machines' transaction capability had been disabled. This made it especially difficult to determine which cards might have been compromised, Zawodniak said.

Boston police in October arrested two Colombian nationals they believe used a skimming device attached to ATM card readers. The rigged ATMs had orange signs in English and Spanish that said: "ATM screen options have changed. Please note the new option before making your selection," an increasingly common tactic with fraudsters.

In Malaysia several banks temporarily suspended their links with the country's Malaysian Electronic Payment System (MEPS) network following a spate of fraud-related cash withdrawals in June in which 397 cardholders in Kuala Lumpur and Selangor lost 1.2 million ringgits (about $316,000 U.S.). Others set lower daily cash withdrawal limits.

While an estimate of fraud losses in Malaysia was not available for 2002, Malaysia lost more than 40 million ringgits (approximately $10.5 million) to ATM and credit card fraud in 2001, up from 28 million ringgits (about $7.3 million) in 2000 and 24 million ringgits (about $6.3 million) in 1999.

Government authorities stepped up a plan to replace magnetic stripe cards with a chip-based Payment Multipurpose Bank Card, which Malaysian newspaper The Star reported would be issued in the first quarter of 2003. The Star said that MEPS expected to convert all of the country's cardholders by April.

C. Arulselvam, country manager for NCR Malaysia Sdn Bhd, anNCRsubsidiary, told The Star that the move to chip will be one of the biggest projects ever handled by NCR in Asia-Pacific, with 2,000 ATM upgrades and another 1,000 new machines.

One Malaysian bank, RHB Bank Bhd, estimated the costs of converting its network of 458 ATMs and one million cardholders to chip technology at 40 million ringgits (about $10.5 million). Peter England, RHB's head of consumer banking, said the bank would replace 75 percent of its ATMs and upgrade the rest.

In Canada, police in December arrested a 34-year-old illegal Russian immigrant allegedly involved in a scam that drained more than $1.2 million from ATMs in Canada and elsewhere. Authorities told the Canadian Press that they believed card data was stolen via a skimming device from three non-bank ATMs in Vancouver over a period of several months.

Police seized 77 cards and about $1,000 from Dimitri Brezinev when they arrested him at a Bank of Montreal ATM.

Police in Australia and Israel also reported multiple incidences of card fraud at ATMs in December. Israel Discount Bank cancelled 3,000 cards and imposed daily cash withdrawal limits on its customers in the wake of a scam. The Daily Ha'Aretz newspaper reported that Israel's National Fraud Squad was exploring the possibility that two suspects arrested while trying to withdraw cash using forged cards were involved in a multi-national crime ring.

Cash out

Another scandal that rocked the ATM industry unfolded in January after Michael Schwartz, a 37-year-old Jersey City, N.J., resident who the FBI said stole $5 million in ATM vault cash, turned up dead on Dec. 25, 2001 in the West Palm Beach, Fla., apartment of Christopher Lacroix, his roommate of less than a month.

Schwartz, the owner of Direct Connect ATM and Schwartz Armored LLC, was last seen by a Jersey City neighbor on Dec. 2, 2001. California-based Humboldt Bancorp, the supplier of vault cash for Schwartz's businesses, reported on Dec. 12, 2001 that it would take an after-tax charge of about $3.1 million to cover losses associated with Schwartz.

Lacroix said he found Schwartz dead on a couch following a drinking binge. He later led authorities to nearly $3.5 million piled in duffel bags on the floor of an abandoned house, as well as $68,000 he had deposited into a safety deposit box in his name.

In March, Lacroix pleaded guilty to charges of receiving, possessing and storing stolen property. In August, a federal judge in Newark, N.J., sentenced him to the maximum sentence of seven years and one month in prison.

The aftereffects of the Schwartz case, combined with soaring insurance costs after the Sept. 11, 2001 terrorist attacks in New York City and Washington, D.C., left many armored car companies struggling to find insurers and paying higher rates when they were able to do so. In a 2001 white paper written by Mike Tawney, executive vice president of risk management forLoomis Fargo, Tawney said that his company expected several of its premiums to rise by at least 100 percent in 2002.

Changing regs

The threat of increased regulation loomed large over the ATM industry in 2002.

MasterCardissued a set of deadlines for implementation of Triple DES (or Data Encryption Standard), a more secure algorithm for encrypting PINs. MasterCard mandated that newly-installed ATMs be capable of running Triple DES by April 1, 2002; networks and host processors must use Triple DES at capable ATMs by April 1, 2003; and all ATMs must be Triple DES compliant by April 1, 2005.

In the wake of much industry angst over the deadlines,Visaand some EFT networks issued slightly different deadlines. Visa wants newly installed ATMs to support Triple DES by Jan. 1, 2003.Star Systemswill require new or replaced ATMs to be Triple DES compliant - not "capable," as in MasterCard's wording - by June 30, 2002. Star wants all transaction hosts and processors to run Triple DES on machines that are capable of doing so by June 30, 2004, and Star's "drop dead" date for all ATMs to run Triple DES is Dec. 31, 2005.

There is a possible silver lining to what promises to be a stormy Triple DES implementation process. Several ATM vendors created Triple DES fixes that will facilitate the automated distribution of the encryption keys that are installed manually into ATMs, an expensive and labor intensive process today. An X9 committee, part of a group led by the American National Standards Institute (ANSI) and the American Bankers Association (ABA) that develops and publishes voluntary technical standards for the financial services industry, is currently working on developing standards for remote key management.

Dates on the way toTDES April 1, 2002All newly-installed ATMs must be triple DES capable. That is, they must be capable of processing Triple DES at the point of interaction. "Newly installed" also includes replaced and relocated ATMs.April 1, 2003All member and processor host systems must use Triple DES in accordance with triple DES requirements for PIN-based transactions that take place at triple DES compliant ATMs. All ATMs installed, replaced or relocated since April 1, 2002 must be triple DES compliant. April 1, 2005All ATMs must be Triple DES compliant. Source: MasterCard Global Deposit Access Operations Bulletin, No. 3, March 29, 2002 |

The federalAccess Boardin April issued a final draft of its proposed revisions to the Americans with Disabilities Act Accessibility Guidelines (ADAAG), after a long process of review following the issuance of a set of proposed changes in November of 1999. As expected, the draft included a requirement for ATMs to be audio enabled.

The good news: The draft wording leaves several options open to ATM vendors, an important consideration given the varying capabilities of different makes and models of ATMs and the diverse needs of deployers.

The draft is now under consideration by the Department of Justice (DOJ), which will ultimately enforce any revisions to the ADAAG. The DOJ is expected to release guidelines in 2003 that will answer two of the most hotly-debated questions, when ATM deployers will be expected to comply and which if any ATMs will be grandfathered.

Several of the nation's largest banks, including Bank of America, Wells Fargo, FleetBoston Financial, Bank One, Citibank and Wachovia, have already rolled out audio-enabled ATMs. In 2002, Washington Mutual and BofA introduced "talking" ATMs that spoke both English and Spanish, and several other banks announced plans for "bilingual" ATMs.

Smooth intro

All was not negative in 2002. The ATM played a key role in the smooth January rollout of the euro, Europe's new common currency. More than 15 billion bank notes and 52 billion coins -- worth 646 billion euros -- were distributed for the switch, many of them at ATMs.

According to press reports, 80 percent of the 12-country euro zone's 250,000 ATMs dispensed euros by Jan. 2. Few glitches were reported, and demand for money from ATMs reached four times the daily average on Jan. 1, according to the European Central Bank. All ATMs were converted to the euro by Jan. 7.

"The number of transactions was a lot higher than predicted, because the ATMs were ready and re-filled a lot quicker than was hoped possible," said Guillaume Lepecq of Agis Consulting, who worked withDe La Ruefor the launch.

Function at a junction

The promise of advanced functionality at the ATM began to happen -- albeit on a still relatively small scale.

Euronet Worldwide, which offers prepaid cell phone top-ups at ATMs in several European countries through partnerships with financial institutions and carriers, signed an agreement to do so in the U.S. withBoston Communications Group (bcgi),a transaction provider to the wireless industry. Several deployers, includingE*TRADE Access, announced their intent to offer the service.

Welch Systems, an NCR distributor, began offering prepaid wireless, along with prepaid long distance and prepaid movie tickets, at about 50 ATMs in the St. Louis area through NCR's iATMglobal program. NCR's partners in the program include bcgi, Radiant Technologies and MCI WorldCom, all of which provide prepaid long distance and/or wireless; online ticket seller movietickets.com and online florist Flowers USA.

Tritonmade Euronet's prepaid wireless one of three applications it is offering to its distributors through its new Waves program, along with money transfer throughWestern Unionand check cashing throughCashWorks, a new company created by several former principals of InnoVentry.

|

Coming soon to an ATM near you? Deployers hope to offer advanced ATM functions such as ticketing, prepaid wireless top-ups and more in 2003. |

After signing agreements with several large ISOs includingCardtronicsandFinancial Technologies, CashWorks was offering check cashing at more than 100 retail locations by December. According to Brian Archer, Cardtronics' executive vice president of marketing, one of his company's best locations cashes more than 600 checks a month.

In July,7-Elevenannounced plans to add 1,000 more Vcom financial services kiosks to the 94 it had deployed previously. If that rollout is successful, the retailer will add another 2,500 locations. The kiosks already offer cash withdrawals, check cashing, money orders and money transfer. 7-Eleven has also lined up partners to offer telecommunications services, e-shopping and auto insurance.

Concord EFSin March announced a partnership withTravelers Express/Moneygramto offer money transfer at ATMs in the Star network, which is owned by Concord.

Consolidation continues

The trend toward consolidation continued, most notably in the network, transaction processing and ATM deployment sectors.

Following its acquisition of the MAC network in 1999 and the Cash Station network in 2000, Concord EFS created the country's largest EFT network -- with 195,000 ATMs, 800,000 point-of-sale locations and 132 million cards -- by purchasing Star in February. Concord also purchasedCore Data Resources, a transaction processor that drives about 35,000 retail ATMs, in March. With the addition of the Core Data ATMs, Concord now drives nearly 95,000 machines.

While Concord established a new, for-profit network dynamic, thePulsenetwork in February created a not-for-profit network with about 81,000 ATMs and 457,500 POS locations by purchasing Tyme, another network owned by its financial institution members.

On the deployer side,eFundspublicly announced purchases of three ISOs in 2002 -- Hanco Systems in February, Samsar ATM Company in May and Evergreen Teller Services in July. Reportedly eFunds purchased another prominent ISO in the Western half of the U.S. in 2002's fourth quarter -- but it has yet to officially announce the deal. Including the as-yet-unannounced deal, eFunds now has nearly 17,000 ATMs under contract and drives about 9,500 of them.

It was also a buyer's market for Cardtronics. The Houston-based ISO, which in 2001 bought a portfolio of about 1,100 ATMs from McLane FSP, in October bought 1,200 retail ATMs from manufacturerDiebold. Cardtronics now has about 9,000 machines under contract, including corporate accounts with the likes of ExxonMobil, Rite Aid and Uni-Mart.

Tough economic times

Unfortunately, both Concord and eFunds experienced financial troubles in the wakes of their buying sprees.

Concord stock, which traded at a 52-week high of $35.06 on May 15 and was still as high as $28.25 on July 12, lost 30 percent of its value in late July and August after its earnings per share slipped from 14 cents in 2001's second quarter to 12 cents in 2002's second quarter. The price took a particularly steep dive after online business site Briefing.com reported that the Securities and Exchange Commission was investigating the company, even though Concord denied the report.

Philadelphia law firm Spector, Roseman & Kodroff filed a class action against Concord on Nov. 1, alleging that Concord had issued false and misleading statements about its business in order to allow Concord stock to trade at artificially inflated levels.

Concord rebounded with a report of record third-quarter earnings of $93.4 million, an increase of about 12 percent from 2001's third quarter -- although Concord president Edward Labry warned of a possible slowdown in business in the earnings release. "September volume was somewhat lower than expected," he said. "This was consistent with the overall slowdown in consumer spending, and we will be closely monitoring the economy's impact on transaction volumes in the coming months."

For eFunds, the problems began in June when the company lowered its earnings outlook for the third quarter and the year, citing downward price pressure in transaction processing, slower-than-expected growth from its ATM management business and delayed buying decisions by several major clients. Also announced was the unexpected departure of chief financial officer Paul Bristow. The stock dropped 30 percent on June 5, closing at $9.32. Its earnings came in at $10.7 million for 2002's third quarter, down 22 percent from 2001's third quarter.

Widening worldview

As the North American landscape began to look a little cluttered with ATMs, vendors looked to other corners of the world for future expansion efforts -- most notably India and China.

In India, Diebold created a new wholly-owned subsidiary, Diebold India Private Limited, and signed a contract manufacturing agreement with the Indian IT firm, Tata Infotech Limited. NCR opened a new manufacturing facility and a professional services facility in Bangalore. NCR chief executive Lars Nyberg said in November that NCR expected to double its workforce in India, to about 1,000 employees, in the next 12 to 18 months.

With nearly 380 million bank account holders but just 7,500 ATMs, India has one of the lowest ATM penetrations in the world.

China was another hot spot, with both Diebold and NCR announcing several multimillion dollar deals with financial institutions there. Retail Banking Research Ltd. predicts that China will become the world's third largest ATM market by 2007; it was the fifth-largest market with some 51,000 machines at the end of 2001.

While China has more than 430 million bank cards in circulation, there is little connectivity between the country's ATMs, and only about 7,000 machines can accept foreign bank cards. However, China's major banks in March established China UnionPay Company Limited, a Shanghai-based network that they hope will allow account holders to use their bank cards at any ATM by 2005.

So what will happen in the world of ATMs in 2003? The only safe prediction: it will -- as always -- be a year to remember.

Included In This Story

Diebold Nixdorf

As a global technology leader and innovative services provider, Diebold Nixdorf delivers the solutions that enable financial institutions to improve efficiencies, protect assets and better serve consumers.

Related Media

Subscribe

Get the latest news and resources from ATM Marketplace.