News

Commentary: Breaking down the break-even

Break-even is the magic ATM transaction number at which revenue covers all expenses and begins to generate income. Not surprisingly, according to a study by KLCI Research, two of the biggest factors impacting break-even are surcharging -- or lack thereof -- and method of cash replenishment.

March 25, 2002 by Peter Kulik — -, Fifth Third Bank Processing

ChatGPT

ChatGPT Grok

Grok Perplexity

Perplexity Claude

Claude |

Peter Kulik |

The business side of deploying ATMs in "convenience locations" is surprisingly consistent around the world. The results of KLCI Research Group's recent worldwide study of "Entry-Level ATM Trends and Futures" showed that in most cases, the decision to deploy an ATM at a site is based simply on the break-even point of the ATM - the transaction volume at which revenue covers all expenses and begins to contribute to income - and the potential transaction volume of the site.

Taken on a broad scale, this result suggests an inverse relationship between the number of ATMs installed in a country or region and the break-even point - as the break-even point is reduced, more deployers will deploy more ATMs, leading to a higher density of ATMs per thousands of population.

The key factors that affect break-even include those associated with revenue, ongoing costs and up-front investment:

· Revenue

· Surcharges or convenience fees

· Interchange revenue

· Operating costs

· Transaction processing

· Cash and cash replenishment

· ATM maintenance

· Support

· Site fees

· Up-front investment

· ATM hardware and software cost (typically leased or depreciated)

· Installation

· Site preparation

· Set-up fees

Based on direct input from among the 37 participating deployers in KLCI's "Trends and Futures" study, two of the most important factors affecting the break-even point are surcharges or convenience fees, and the approach to cash replenishment.

|

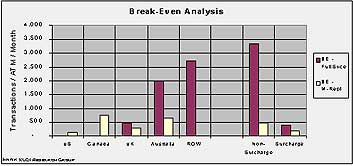

The average break-even point ranges from a low of 200 transactions a month at merchant-replenished sites in the United States to more than 3,000 transactions a month at full-service cash replenishment sites in countries where surcharges are forbidden.

Some key conclusions:

· It should not be a surprise that the United States has the highest number of ATMs per thousands of population - it has the lowest break-even point for ATMs in convenience locations.

· Surcharging makes a dramatic difference - in non-surcharging countries, participants' break-even points averaged approximately 3,000 for full-service installations, compared to less than 500 for full-service installations in countries with surcharging.

· Merchant replenishment is a significant cost reduction. Costs of cash and cash replenishment are typically the largest single component of ATM operating costs - around one-third of the total, based on KLCI Research Group studies; the break-even point for merchant replenishment can be as low as 200 transactions per ATM per month.

Other factors affecting the break-even point may come into play on a local basis, such as the cost of complying with security requirements in some countries, which participants reported can drive the average break-even point to 4,000 transactions per ATM per month or higher.

How low can the break-even point go? Site rental fees (where applicable) and ATM lease or depreciation are the only fixed costs in the lists above - all other costs will rise and fall with transaction volume, to a greater or lesser extent.

ATM Manufacturers have continued to reduce the cost of ATM hardware and software, so lease or depreciation costs have continued to decline. The bottom will probably be determined by point-of-sale debit - the point at which giving "cash back" at the time of purchase is more attractive to merchants than installing an ATM, in countries where this practice is common.

There is also the potential to increase the revenue from ATM installations with new transactions, or advertising, or both. Increasing revenue will reduce break-even points, but some approaches are better than others - and no transactions are as promising as cash withdrawal. More about this in a future column.

KLCI Research Groupis a market research firm with focus on the Financial Services, ATM, and Kiosk industries.Recent studies have included "ATM Industry Operations and Cost Benchmark," "Entry-Level ATM Trends and Futures," "Reducing Costs of ATM Cash" and the Kiosks.org RFI Analysis.

With more than 15 years experience in the financial services industry,Peter Kulikhas published and spoken widely on topics ranging from ATM Operations to Outsourcing to CRM.He is Managing Director of KLCI Research Group, and focuses on research for banking and independent ATM deployment.Some recent clients have included CIBC, Halifax plc, NCR, and RBC Royal Bank; he also spoke on CRM in the ATM Channel at the 2001 BAI RDS conference.

Related Media

Featured Vendor

![]()

Auriga is a top international software solutions company, specialized in end-to-end systems that integrate the various delivery channels used in retail and internet banking.

Subscribe

Get the latest news and resources from ATM Marketplace.