News

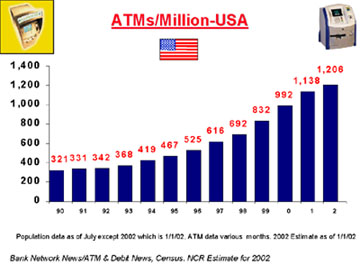

An ATM for every 1,200 Americans

NCR's Bill Koch believes that even though the U.S. has the world's second-highest ratio of ATMs per capita, the growth in ATM locations will continue.

October 24, 2002

ChatGPT

ChatGPT Grok

Grok Perplexity

Perplexity Claude

ClaudeThe United States' ATM market has been transformed from a slow-growing market that bought 10,000 ATMs annually (1987-1992) to a dynamic market with five times such shipments (1997-2001). Who could have foretold this in 1992, after 20-plus years of ATMs in America? At that point we had an installed base of 94,822 ATMs. Americans have purchased more than 300,000 units in the succeeding nine years.

|

Bill Koch |

At the end of 2001, there were between 345,000 and 350,000 ATMs in the U.S. On the basis of the latest population figures produced by the Census Bureau, this equates to more than 1,200 ATMs/million. Only Japan can claim a higher ratio, and according to Retail Banking Research estimates, the comparable figure for Western Europe was 553 ATMs per million population at the end of 2000.The global figure is just under 200 ATMs per million population. What do such indicators signify? Of course they are not a perfect reflection of the level of convenience provided to customers. The crude ratios take no account of location (geographic spread), hours of opening or the number of customers served. But they are the best measure we have.

So why is the U.S. so high in this measure? It has grown from an also-ran to near the top of the heap. A major factor in the rapid U.S. growth has been surcharging -- a fee that the ATM owner charges the cardholder directly for the convenience of using his ATM. Surcharging is market-based pricing determined by the ATM owner who sets the price and the cardholder who accepts or rejects it.

|

While surcharging is certainly key, it by no means explains the whole picture. If this were the only reason, I suspect that the U.S. would have stopped somewhere in the 200,000 range of ATMs. The fuel that continues to fire the latest growth in the installed base is a new model of operation as well as an additional justification for ATMs.

New methods

In the U.S., service providers (generally called ISOs) provide ATM programs that allow retailers to own (or more typically lease) ATMs and operate them. These service providers have learned how to operate an ATM cost efficiently in conjunction with retailers.

How are they more efficient? The ISOs operate on a low-cost model that has a number of key elements:

- They contract to buy ATMs in bulk to get the best price.

- They buy inexpensive ATMs meant for low-volume locations.

- Safes, cameras and other security measures may be substantially less than bank ATMs due to regulation and business needs. For example, a retailer does not have to conform to the Bank Protection Act, and the retailer may put less cash in his ATM.

- They use dial-up communications with the host that drives them, a more sensible communications method in low-volume situations.

- They often have substantial merchant involvement in the operation of the ATM.

The merchant could:

- Own the cash in the ATM.

- Reload the cash (typically enough for a day). If the store is not 24 hours, he may remove the cash at the end of the day for safekeeping in the store vault.

- Handle simple repairs such as clearing jams of cash or receipt paper.

- ISOs work hard to help the retailer resolve as many problems over the phone versus sending a technician to fix the device. They do this since it brings the machine back up more quickly and saves money all around.

- Non-bank uptime standards may not be as demanding as banks since they typically make trade-offs of cost of servicing versus uptime. Examples can include less monitoring of ATMs and next-day service. Banks are generally very cognizant of their uptime since typically they have their most valuable asset -- their brand on the ATM. A merchant may see the machine as a vending machine for cash but a bank may see it as its main business.

Alternative Approaches

It is typical for chain stores to opt for a "turnkey" method of operating. By this I mean that the site owner has little involvement in the operation of the ATM. The chain relies on more typically a bank but occasionally an ISO for this service. My sense is that the chains don't want cash control and liability issues than can come with ATMs. They want store management to focus on the business of running a store. In contrast, the independent storeowner has fewer worries concerning cash control since often the people who load the cash are the shop owners. In addition, the independent wants an ATM because he feels that it will add more profits to his bottom line.

Key Drivers

One of the other key drivers to this movement is the belief that an ATM can increase store sales. Any time it is easy for people to get cash, a percentage will do so, even if it means paying extra for the convenience. In fact, Bank Rate Monitor estimates that in the U.S., in 2001, consumers paid $2.2 billion in surcharges. At their average surcharge of $1.45, this means that American consumers paid a surcharge over 1.5 billion times last year. Why? It is simply a trade off of time versus money (convenience). This is also why more than 91 percent of the ATMs in the U.S. surcharged as of the end of 2001.

In the time-compressed world in which many people now live, having an ATM in a store makes one more inclined to go to that shop. In such businesses as convenience stores where some street corners may have more than one shop, an ATM can be a competitive advantage. Evidence suggests that consumers get into the habit of going to the location with the ATM even when they don't need cash! Never underestimate the power of habit. The consumer gets into the habit of going to the convenience store with an ATM to get his twice-weekly allotment of cash and returns when he wants fuel or a hot or cold drink.

Another element of consumer behavior can also drive sales revenue. When consumers have more cash in their hands they are more inclined to spend some of it on site. According to a survey done by a U.S. ISO and reported in Convenience Store Decisions in May 1999, ATM users spend 25 percent more than non-users. My advice to ATM owners is to do a little survey to confirm and measure the phenomenon.

In summary, increased sales can arise from the draw of the ATM, a resulting change in shopping behavior (habit) and the tendency for consumers to spend more when they have cash in hand. How big an impact will these factors have on sales? Obviously it will vary by situation. It may be small in percentage of store sales in a giant hypermarket like a Wal-Mart Supercenter, but a bigger number in a bar or C-store.

In the U.S. C-stores, the sales increase may be in the 1-3 percent range. I have heard and read higher numbers such as those in the 5-10-plus percentage range. Obviously a number of factors come into play such as the position of the ATM in the store, promotion, signage, uptime, the competitive situation, etc. There are no definitive numbers in the U.S. I have, however, created a model based on U.S. C-Store trade data that suggests that with a 2 percent increase in in-store sales, the average C-Store's bottom line before tax increases 8 percent.

In other markets with fewer ATMs, the sales increases can be much higher. One privilege I have had in working for NCR is the chance to travel to markets outside the U.S. I can remember retailers telling me of increases from 10-30 percent in the store's business due to an ATM. This is an incredible range to me, a conservative ex-banker. My thought is that in such cases, the ATM must become a significant reason for customers to visit such stores and that such countries don't have enough ATMs.

Where will it stop? I hate to underestimate the power of ATMs and the free market. Most experts have consistently underestimated the growth of the U.S. market. My sense is that in the U.S., even with its high number of ATMs/million, the installed base will continue to grow until ATMs are indeed virtually everywhere where they make economic sense. In addition, I believe that many of the markets of the world have the elements that are necessary to follow a similar but probably country specific path to more ATMs. It reminds me of what I am sure is an anecdotal story of two shoe salesmen who were sent to Africa at the end of the 19th century. One cabled back, "Bring me home -- nobody wears shoes." The other wired back, "I don't want to go home -- nobody wears shoes!" Remember the ATMs/million figures for the U.S. at more than 1,200 versus the same ratio for Western Europe at 553.

Related Media

Subscribe

Get the latest news and resources from ATM Marketplace.